In earlier days, we used to visit nearby shops, compare prices from one shop to another, and sometimes postpone purchases due to a money shortage. We had to put effort into buying, as every transaction was in cash, and spontaneous buying was rare. This is not because we had self-control, but because choices were limited.

Now, the world has changed – a few taps on a mobile phone, we get food, clothes, gadgets, and subscriptions. What was once carefully planned is now immediately available. Even school students can purchase or influence purchases anytime and anywhere. The responsibility of managing money has become much greater, especially for young learners. This makes financial literacy for students essential.

Read More: Why is financial literacy an essential part of education?

What Is Financial Literacy?

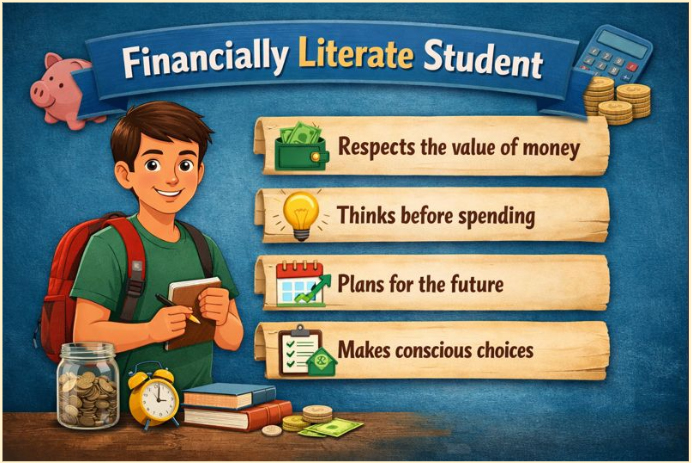

Financial literacy is the capability to understand money, manage it, and make responsible financial decisions.

For a school student, being financially literate means knowing how to maintain pocket money till the month end, understanding why saving is difficult but essential, and realising that every rupee carries effort behind it.

Why Financial Literacy For Students Matters More Than Ever

Earlier generations learned financial orderliness naturally through limited options, family discussions, and careful planning. Today’s students, however:

- Make independent purchase choices early and independently

- Face constant temptation through offers and trends

- Have access to digital payments and immediate buying

- Realise too late how quickly small expenses add up

These habits can lead to confusion and later regret if there is no proper guidance. Financial literacy helps students to think before spending and to think beyond the moment.

Read More: Challenges of Technology in Education

Core Principles of Financial Literacy

A strong financial understanding for students is built on simple principles:

- Mindfulness before spending: The first step to control is to understand where money comes from and where it goes.

- Needs before wants: To learn to choose essentials over wants.

- Saving as a habit: Saving regularly, not occasionally.

- Thinking ahead: Thinking beyond today’s purchase in every decision.

- Responsibility and discipline: Every money decision comes with a responsibility for its result.

Bringing Financial Literacy to Life in the Classroom

We found that students learn best when money lessons connect to real life. So teachers brought it to life through stories, discussions, and activities.

1: Start with What Students Know

- Relate lessons to situations students already know:

- Pocket money management

- School trips and expenses

- Buying gadgets or books

2: Ask Questions That Make Students Think

- Why did you choose to spend or save?

- What would you do differently next month?

3: Extend Learning Beyond School

- Encourage students to:

- Discuss household budgeting with parents

- Observe real-life financial decisions made at home

Financial Literacy Examples

To make learning more meaningful for students, schools can use financial literacy examples from real educational settings. Activities like budgeting for a school event, planning savings for a class project, or understanding how schools manage resources help students relate to real life. When students understand that even institutions must plan, save, and borrow responsibly, financial literacy becomes more relatable and practical. Here are a few practical financial literacy examples that can be done in the classroom.

| Activity | What Students Do | How the Teacher Can Conduct It | Learning Outcome |

|---|---|---|---|

| Pocket money tracker | Record every money received and spent in a month. | Provide a tracking sheet with columns: Date, Item, Amount, Reason. Explain that the right data is required. Review weekly in short discussions. Ask students to think about spending patterns. |

Mindfulness of spending habits and self-reflection |

| Needs vs. Wants – debate | Differentiate expenses as needs or wants and defend their choices. | Divide the class into 2 to 3 groups. Give each group a list of items (food, phone recharge, branded shoes, outings, etc.). Each group presents and justifies its categorization. |

Critical thinking and prioritization |

| Savings goal planner | Choose a relevant goal and plan how to save for it. | Ask students to choose a realistic/ relevant goal. Break the total cost into weekly or monthly savings. Discuss challenges faced and ways to stay on track. Track progress at regular intervals. |

Patience, discipline, and planning |

| Smart shopping exercise | Compare prices, offers, and value before selecting | Show various price alternatives for the same item (online/ offline, offers, discounts, etc.). Ask students to choose the best possibility and to give reasons. |

Reflective decision-making |

Benefits of Teaching Financial Literacy Early

For Students:

- Better money habits

- Increased confidence

- Reduced impulsive spending

For Schools:

- Life-ready learners

- Stronger parent engagement

What Does It Mean to Be Financially Literate?

As teachers often say, “In a world where spending is easy, wisdom lies in knowing when to stop.”

In the school ecosystem, access to the best loan providers for schools, such as Varthana, highlights how thoughtful financial planning supports infrastructure, learning facilities, and long-term growth. Thus, it reinforces the importance of informed money decisions at every level.

Also Read: The Benefits of Teaching Financial Literacy to Children at an Early Age

Conclusion: From Then to Now

Earlier generations learned financial discipline through limitations. Today’s students must learn it through education and awareness.

By teaching financial literacy for students, it bridges the gap between past perceptions and present realities. Thus, preparing students not just to earn money but to manage it wisely. Access has changed, but responsibility remains the same.

FAQs

1. What are the most important financial skills students should learn?

- How to budget wisely

- Distinguish between needs and wants

- Save regularly, plan for future goals

- Take responsibility for their financial decisions

2. How can parents help improve their children’s financial literacy at home?

- Involving them in everyday money decisions

- Encouraging saving habits

- Discussing needs versus wants

- Modelling responsible spending

- Open conversations about money

3. Which financial literacy apps are best suited for Indian students?

- MoneyView – Tracks expenses, bills, and budgets in one place and sends reminders. For students starting to manage money independently.

- Goodbudget – Uses the envelope budgeting method to help students place money into categories like food, travel, or savings and maintain limits.

- Money Manager / Money Manager Expense & Budget – It is a manual tracking with visual charts. Helpful for students who prefer hands-on budgeting.

- Walnut – Automatically tracks spending by reading SMS alerts. For beginners, managing pocket money and monthly expenses.

4. At what age should financial education begin?

It should begin as early as 6–8 years of age, when children start handling money. The concepts grow gradually as they move through middle school to high school.

5. How can schools integrate financial literacy into their existing curriculum?

By including money-related concepts in subjects like Mathematics, Social Science, Life Skills, and Economics. By using real-life examples such as budgeting, saving, and decision-making. Through activities like projects, discussions, role plays, and case studies. Thus, reinforcing learning without adding a new subject.

6. What are some easy financial literacy examples students can practice daily?

- By tracking pocket money expenses

- Planning a simple weekly budget

- Choosing needs over wants while shopping

- Saving a small fixed amount regularly

- Comparing prices before buying

- Reflecting on spending decisions to understand what could be improved next time

Social